2026 Non-Registered Accounts Guide

A non-registered account is essentially an investment account that isn't tied to a specific government program. Because it’s not "registered," it allows you to invest in pretty much whatever you want—stocks, ETFs, bonds, and mutual funds—without a ceiling.

The catch? It’s a taxable account, meaning whenever you make money, you have to tell the CRA about it at the end of the year.

This is not financial advice; readers must do their own due diligence!

A Canadian non-registered account offers unlimited contribution room and total freedom to withdraw cash whenever you want, making it the perfect "overflow" bucket once your TFSA and RRSP are full.

2. The Features: Ultimate Flexibility

1. What is a non-registered account?

This account is all about freedom. You have zero contribution limits, so you can invest $100 or $1,000,000 if you've got it. There are also no withdrawal restrictions, so if you need to pull money out for a last-minute trip or a car repair, you can do it whenever you want.

You can set this up as an individual account or a joint account with a partner if you're building a life together. Whether you want to be a self-directed trader picking your own stocks or use a managed portfolio to do the work for you, the choice is yours.

Unlike your TFSA (which is a tax-free gift) or your RRSP (which kicks the tax can down the road), this account is taxable every single year. You’ll be taxed on:

Capital Gains: When you sell a stock for more than you paid.

Dividends: Those sweet little payouts companies give you for holding their stock.

Interest: What you earn on bonds or cash.

Pro Tip: You have to track your Adjusted Cost Base (ACB). Since we're in 2026, keep in mind that if you get lucky and net more than $250,000 in capital gains in a single year, the inclusion rate jumps from 50% to 66.7%. Even if you just sell to "rebalance," that triggers a taxable event.

3. The Tax Man: How it Works

The Good Stuff

The main vibe here is unlimited space. It’s the perfect "overflow" bucket once your other accounts are full. It works for literally any goal—short-term or long-term—because you aren't locked into any government retirement timelines.

The Reality Check

There is no tax shelter, so your gains will be trimmed by the CRA. It also requires more "adulting" because you have to track your buys and sells for tax season, making it a bit more complex than your standard TFSA.

General rule of thumb: Max out your TFSA, FHSA, and RRSP first. You should only really be looking at a non-registered account if those three are already full. It’s the best move for extra investing when you’ve hit your limits but still want to grow your wealth or keep your money flexible.

4. The Pros and Cons

5. When Should You Actually Use This?

Keep your strategy simple and consistent. Focus on long-term ETFs rather than trying to day-trade your way to a tax headache. Be mindful of taxes; the less you "buy and sell," the less you have to pay the government in the short term. Apps like Wealthsimple make this easy by offering commission-free trading and automated portfolios so you don't have to overthink it.

6. Pro Strategies

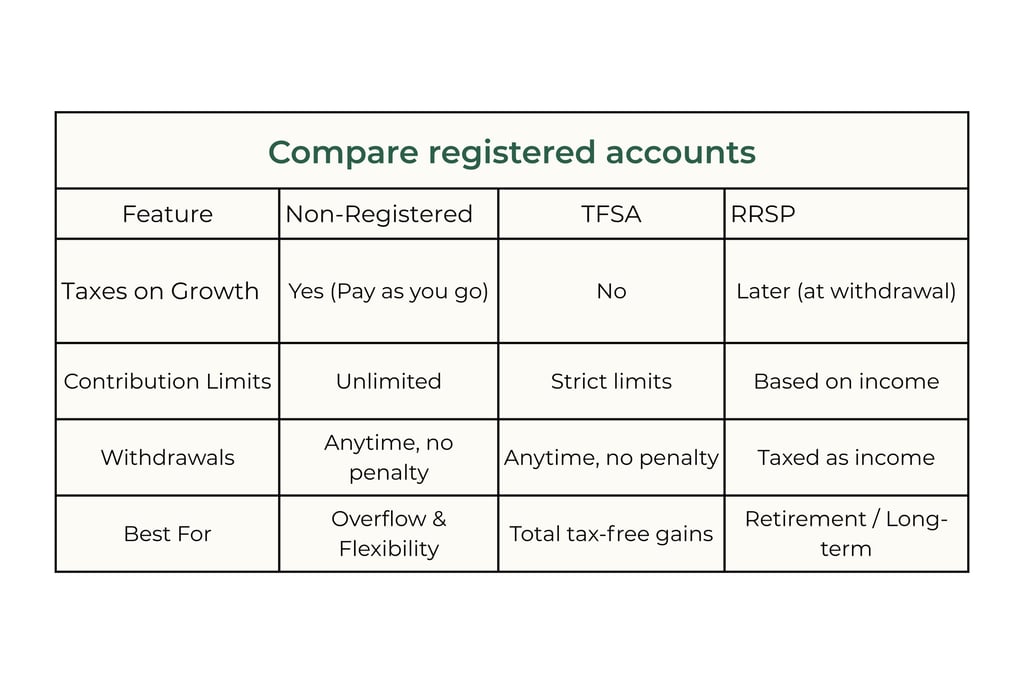

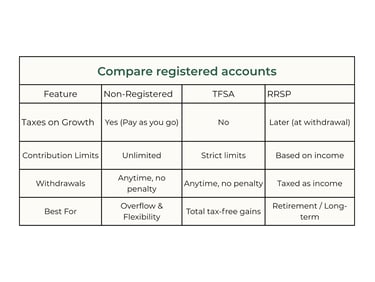

7. The Comparison Table

8. How to Get Started

Opening one is usually easier than ordering pizza. If you're using an app like Wealthsimple:

Log in and hit “Open account.”

Choose Non-registered.

Decide if it’s just for you or a joint account.

Pick Self-directed (if you want to pick the stocks) or Managed (if you want an algorithm to handle it).

Requirements: You just need to live in Canada, have a SIN, and be the age of majority in your province.